In our view, a key reason why well-managed companies like Augusta Gold (TSX: G), Borealis Mining (TSXV: BOGO), and North Peak Resources (TSXV: NPR) remain dramatically undervalued is due to the negative shadow cast by i-80 Gold (TSX: IAU)—a company that, despite boasting a large resource base, has been a disaster in execution.

On paper, IAU may appear to hold more gold resources than Augusta. However, Augusta is likely to surpass IAU’s market cap—despite IAU’s attempt to become a producer, which has turned into a financial sinkhole. Over the past year, IAU generated just $50.34 million in revenue yet reported negative free cash flow of -$84.52 million and now sits on net debt of -$173.08 million, largely owed to unfriendly stakeholders. A bankruptcy appears likely.

Compare this with Titan Mining (TSX: TI)—run by the same leadership team as Augusta Gold. Titan’s zinc mine in New York produced $64.3 million in revenue over the past year, with positive free cash flow of $12.47 million, and a 28.4% reduction in net debt last quarter to a six-year low.

Now imagine that same management team applying their expertise to oxide gold mining in Nevada—a much simpler and lower-risk endeavor than underground zinc mining in New York. If Augusta Gold successfully brings its Reward and Bullfrog projects online, we estimate annual revenues could reach US$500 million, with exceptional profitability.

Following Triple Flag’s CAD$421 million acquisition of our Orogen Royalties (TSXV: OGN), a buyout of Augusta seems imminent. But Augusta’s low share price remains the main obstacle—no acquirer wants to risk offering a 300% premium that could cost their CEO his job. Ironically, Augusta could likely achieve a fairer valuation as a private company—where it could sell the Bullfrog and Reward assets for full value without market distortions.

We’ll admit it—we were too focused on waiting for Solaris Resources (TSX: SLS) to be acquired before highlighting Lumina Gold (TSXV: LUM). That’s on us. We missed the timing.

Still, we wouldn’t mind seeing Augusta sell its key assets at a large premium, then reinvest the capital to make strategic acquisitions. Could Augusta soon be buying i-80’s assets at distressed prices? It’s a real possibility. Rick Rule recently suggested that Equinox should sell Castle Mountain after it finishes acquiring Calibre. That’s just his opinion, of course—but his insights often prove prophetic.

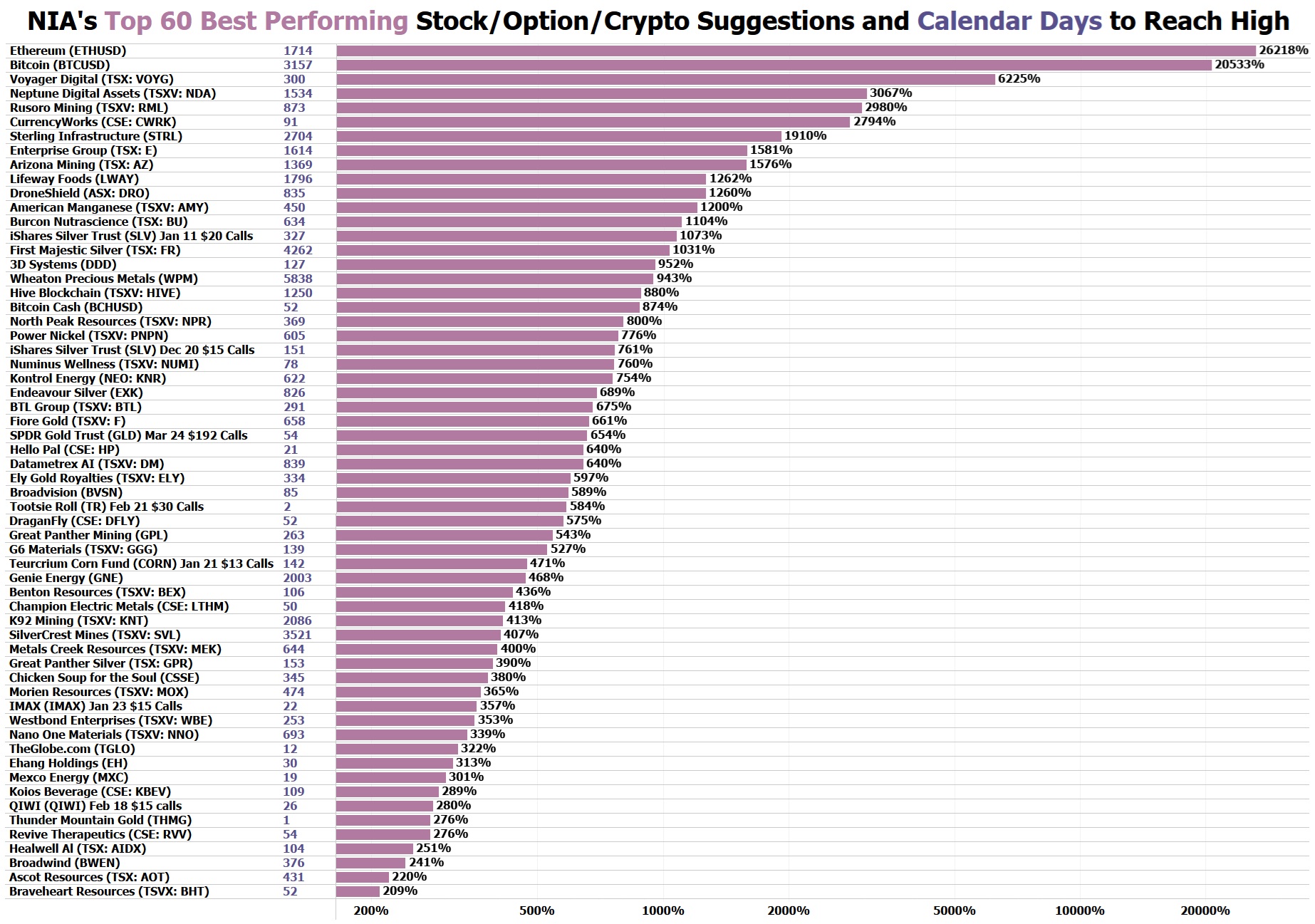

It’s worth noting that Augusta’s Executive Chairman Richard Warke was involved in Castle Mountain’s early development. If anyone knows whether it’s worth regaining, it’s him. What about Calibre’s Pan Mine, which Equinox will soon control? The Pan Mine—previously owned by Fiore Gold—was acquired by Calibre at a 661% premium above our original Fiore Gold suggestion price. Unlike IAU, Equinox is backed by the highly respected Ross Beaty, also the driving force behind Lumina Gold. While they’re unlikely to sell these assets cheap, Beaty may see the logic in securing exposure to the Beatty Gold District, especially after Triple Flag's latest move.

As for Borealis Mining (TSXV: BOGO), their CEO understands what’s at stake. Production begins June 9th, and his goal is to deliver positive cash flow from the outset. Tony Makuch stepping down as Chairman wasn’t a surprise—he’s exited all other board positions to focus on Discovery Silver, now in control of the Porcupine Mine Complex. His replacement, Robert Buchan, founder of Kinross Gold, is an ideal fit to guide Borealis forward.

Let’s not forget: Makuch was the final CEO of Kirkland Lake Gold, which merged with Agnico Eagle (AEM). But it’s Brian Hinchcliffe, the original founder and CEO of Kirkland Lake, who is now Executive Chairman of North Peak Resources (TSXV: NPR).

NPR’s Prospect Mountain Mine Complex, located directly south of i-80’s most valuable holdings, is emerging as a major high-grade play. Recent drill results show game-changing potential:

PM24-039 intersected 22.9m @ 12.0 g/t Au, including 3.0m @ 85.7 g/t Au, suggesting a new Western mineralized trend.

PM24-004 returned 126.5m @ 1.06 g/t Au from surface, indicating continuous low-grade gold between previously unconnected zones—something never outlined by European American Resources (EPAR) in their 1998-1999 campaign.

NPR is like a Highlander Silver (CSE: HSLV)—except it’s based in Nevada with near-term exploration upside and infrastructure already in place.

Past performance is not an indicator of future returns. NIA is not an investment advisor and does not provide investment advice. Always do your own research and make your own investment decisions. NIA's President has purchased 232,200 shares of G and may purchase more shares. NIA's President has purchased 125,000 shares of HSLV and can buy or sell shares at any time. NIA's President has purchased 60,000 shares of NPR in the open market and may purchase more shares. NIA has received compensation from NPR of US$50,000 cash for a six-month marketing contract. NIA has received compensation from BOGO of US$100,000 cash for a twelve-month marketing contract. This message is meant for informational and educational purposes only and does not provide investment advice.

Preparing Americans for Hyperinflation