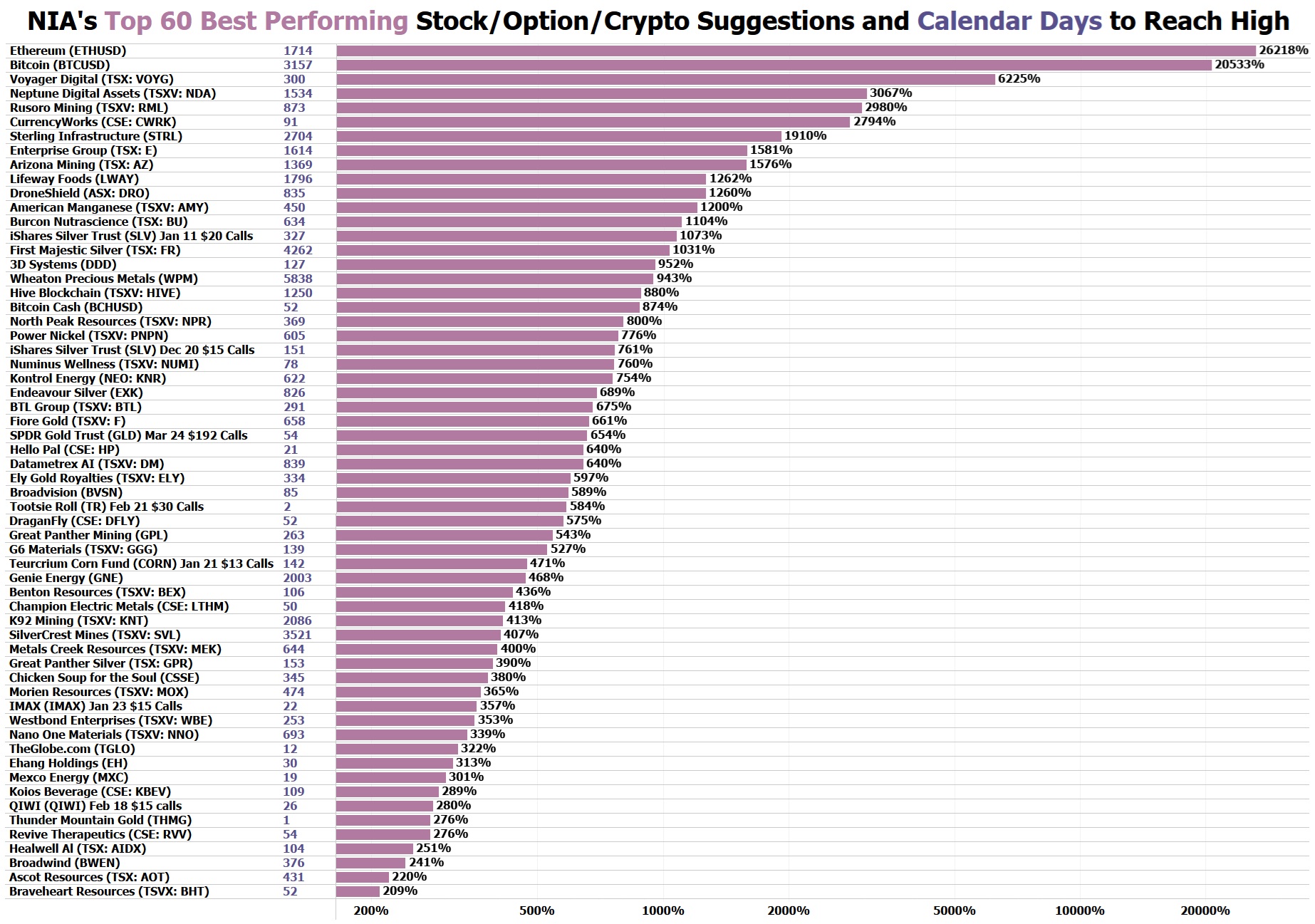

NIA's #1 favorite nickel stock suggestion Power Nickel Inc (TSXV: PNPN) hit a new 6-month high on Wednesday of $0.29 per share for a gain of 28.89% since NIA's suggestion this summer at $0.225 per share.

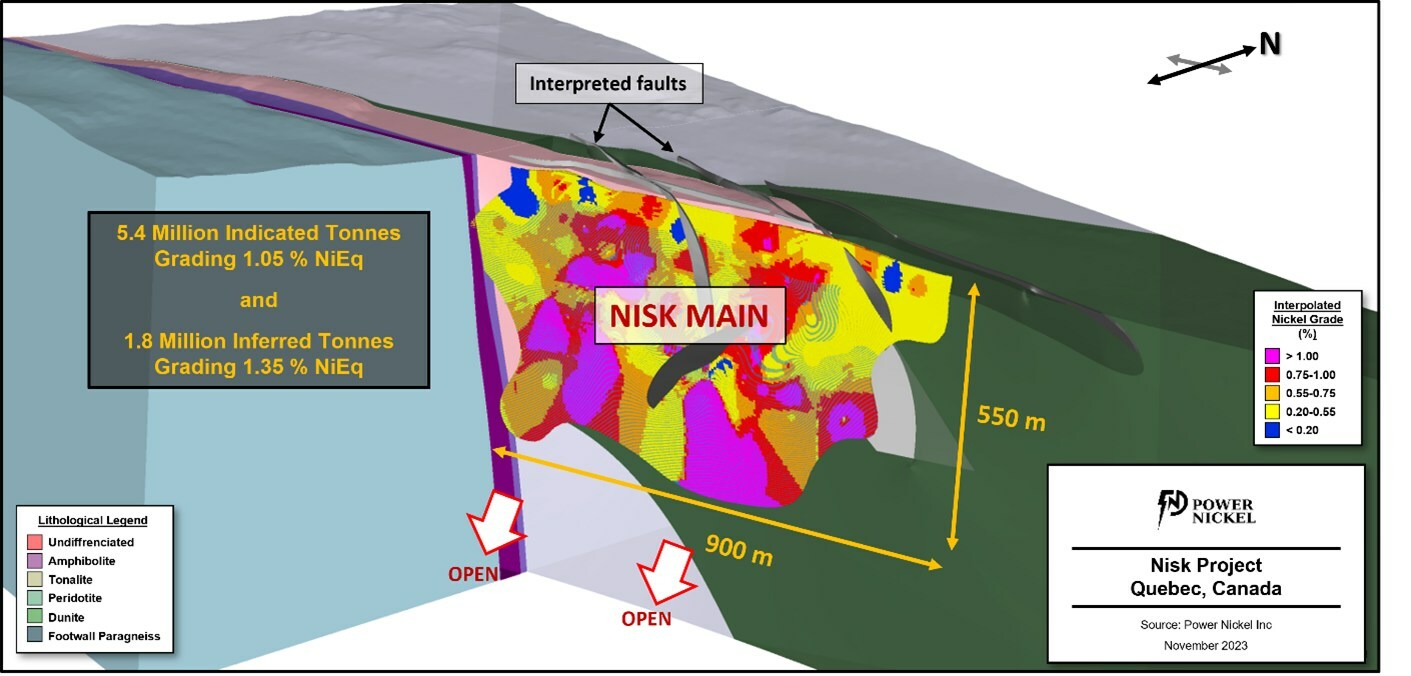

TORONTO, Nov. 29, 2023 /CNW/ - Power Nickel Inc. (the "Company" or "Power Nickel") (TSXV: PNPN) (OTCBB: PNPNF) (Frankfurt IVV) is pleased to release the initial NI 43-101 Mineral Resource Estimate on its "NISK" Nickel Sulphide project, located near Nemaska, James Bay, Québec.

Following up a successful drilling campaign in summer of 2023, and new inputs from the recently completed FLEET Ambient Noise Tomography survey, the Nisk geological interpretation has reached a higher level of understanding, resulting in the elaboration of a robust 3D litho-structural model. This new model is fully integrated to and is constraining the current Mineral Resource Estimation ("2023 MRE").

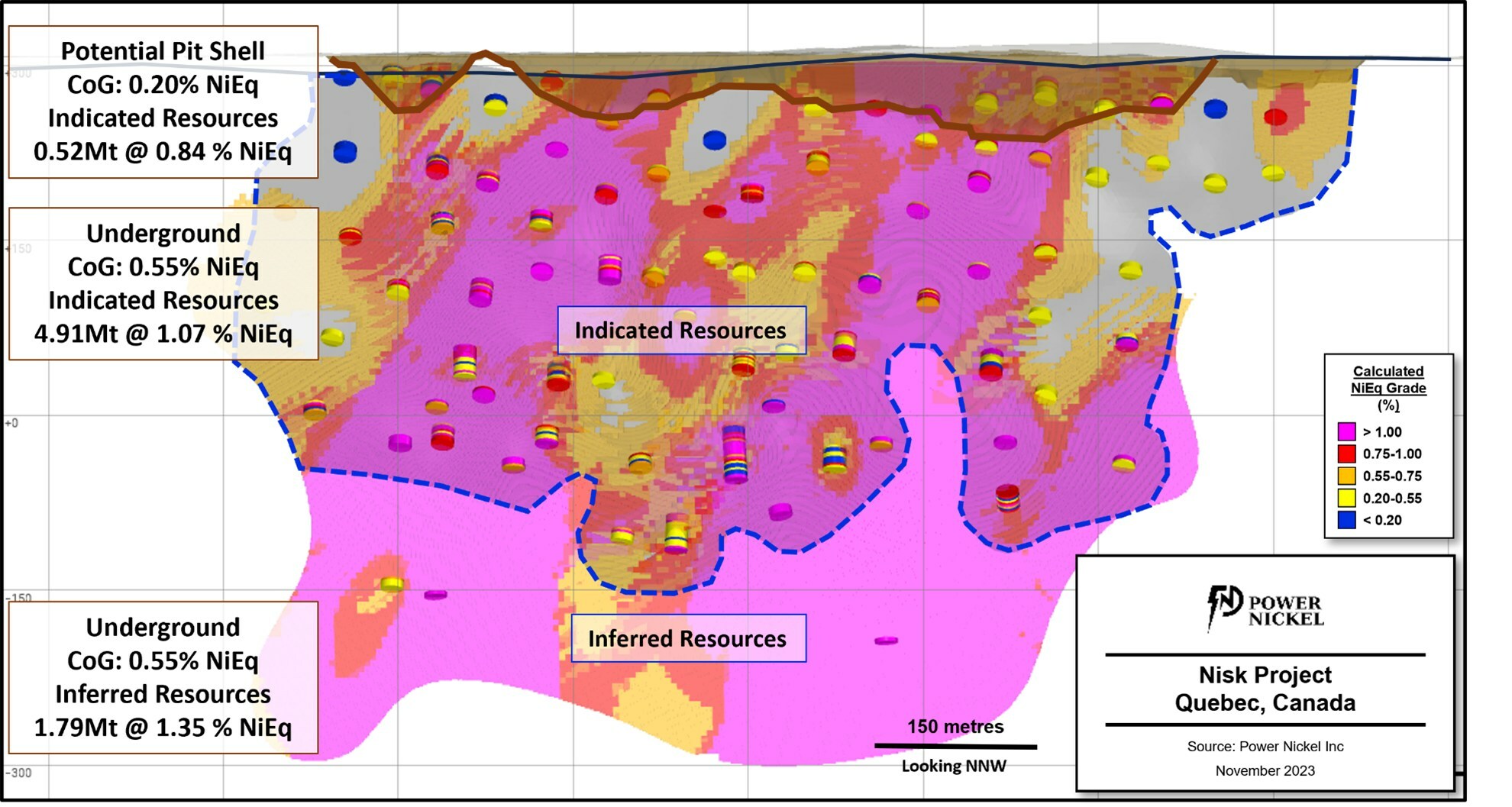

Power Nickel is proud to announce 5.43M tonnes of indicated resources at a weighted average grade of 1.05 % NiEq and 1.79M tonnes of Inferred resources at a grade of 1.35 % NiEq, using a NiEq cut-off grade of 0.20% inside the open pit and 0.55 % for the underground portion.

Power Nickel has retained a group of independent Qualified Persons to perform the 2023 MRE study. The Technical Report will be filed on SEDAR within 45 calendar days. While the oversight of the Technical Report preparation is being undertaken by Duncan Studd, P.Geo (from GeoVector Management Inc.), the Data Validation and Mineral Resource Estimation items were carried out by Pierre Luc Richard, P.Geo (from PLR Resources Inc), on the basis of a metallurgical study performed by Gordon Marrs, P.Eng (from XPS – Expert Process Solutions, a Glencore company) and a pit shell that was generated to constrain the Mineral Resources provided by Jeffrey Cassoff, P.Eng. (from BBA Inc.).

The Mineral Resource Estimate presented herein in Table 1 is either constrained within a pit shell developed from a pit optimization analysis or presented as underground mineral resources using an appropriate cut-off grade and reasonable potential mining shapes which include must-take material.

Table 1 - 2023 Nisk Project Mineral Resource Estimate at a cut-off grade of 0.20% NiEq for the open pit potential and 0.55% NiEq for the underground portion.

|

Potential Mining Method |

In-Situ Grade |

Calculated |

||||||

|

Class |

Tonnage |

Ni |

Co |

Cu |

Pd |

NiEq |

||

|

t |

% |

% |

% |

g/t |

% |

|||

|

Indicated |

Open Pit |

519,000 |

0.63 |

0.04 |

0.30 |

0.56 |

0.84 |

|

|

Underground |

4,910,000 |

0.78 |

0.05 |

0.42 |

0.78 |

1.07 |

||

|

Inferred |

Underground |

1,787,000 |

0.98 |

0.06 |

0.45 |

1.11 |

1.35 |

|

|

Potential Mining Method |

In-Situ Material Content |

Calculated |

||||||

|

Class |

Tonnage |

Ni |

Co |

Cu |

Pd |

NiEq |

||

|

t |

t |

t |

t |

t |

t |

|||

|

Indicated |

Open Pit |

519,000 |

3,300 |

200 |

1,600 |

9,400 |

4,400 |

|

|

Underground |

4,910,000 |

38,300 |

2,400 |

20,500 |

123,100 |

52,300 |

||

|

Inferred |

Underground |

1,787,000 |

17,500 |

1,100 |

8,100 |

64,000 |

24,100 |

|

|

Notes to Table 1: |

|

|

1. |

The independent qualified persons for the 2023 MRE, as defined by National Instrument ("NI") 43-101 guidelines, are Pierre-Luc Richard, P.Geo. of PLR Resources. Jeffrey Cassoff, P.Eng. of BBA is the independent qualified person for the Pit shell analysis and cut-off grade calculations. Gordon Marrs, P.Eng. of XPS is the independent qualified person for Metallurgy and Smelter Costs. The effective date of the 2023 MRE is November 26, 2023. |

|

2. |

These mineral resources are not mineral reserves as they do not have demonstrated economic viability. The quantity and grade of reported Inferred Mineral Resources in this MRE are uncertain in nature and there has been insufficient exploration to define these Inferred Mineral Resources as Indicated or Measured; however, it is reasonably expected that the majority of Inferred Mineral Resources could be upgraded to Indicated Mineral Resources with continued exploration. |

|

3. |

Mineral resources are presented as undiluted and in-situ for an open-pit and underground scenario and are considered to have reasonable prospects for economic extraction. Reasonable potential mining shapes were modeled, and must-takes were included. The constraining pit shell was developed using overall pit slopes of 45 degrees in bedrock and 25 degrees in overburden. Mineral resources show sufficient continuity and isolated blocks were discarded. |

|

4. |

The MRE was prepared using Leapfrog Edge version 2023.2.0 and is based on 117 surface drillholes and 3,835 samples, of which 96 drillholes were intercepting in the Nisk Main Zone. The cut-off date for the drillhole database was November 26, 2023 with hole PN-23-036 being the last hole being included. |

|

5. |

The MRE encompasses one mineralized zone defined by a constraining solid with a minimum true thickness of 2.0 m. A value of zero grade was applied where core has not been assayed. |

|

6. |

High-grade capping was done on the composited assay data. Capping grades are as follow: 2% for Nickel, 1.5% for Copper, 0.15% for Cobalt, 1.2 g/t for Platinum, and 3 g/t for Palladium. |

|

7. |

Density values were calculated for the Main Zone from the density of the host rock, adjusted by the amount of Nickel as determined by metal assays. A formula was calculated and validated using a database of measured densities. Country rock density vary from 2.70 g/cm3 to 2.85 g/cm3. The Main Zone density vary from 2.63 g/cm3 to 3.96 g/cm3. |

|

8. |

Grade model mineral resource estimation was calculated from drillhole data using an Ordinary Kriging interpolation method in sub-block model using blocks measuring 5 m x 5 m x 5 m in size. |

|

9. |

Nickel equivalency grade was calculated using metal prices (see below), metallurgical recoveries, smelter payables and charges. Metallurgical recoveries are 70% for Nickel, 44% for Copper, 79% for Cobalt, and 67% for Palladium. Payables are 73% for Nickel, 69% for Copper, 27% for Cobalt, and 78% for Palladium. NiEq = Ni grade + (0.2359 x Cu grade) + (0.9388 x Co grade) + (0.1810 x Pd grade) |

|

10. |

The estimate is reported using a NiEq cut-off grade of 0.20% for open-pit mineral resources and 0.55% for underground mineral resources. The cut-off grade was calculated using the following parameters (amongst others): Nickel price: USD10.00/lb; Copper price: USD4.00/lb; Cobalt price: USD22.50/lb; Palladium price: USD1,215.00/oz; CAD:USD exchange rate = 1.30. The cut-off grade will be re-evaluated in light of future prevailing market conditions and costs. The pit shell optimization used the same parameters. |

|

11. |

The pit shell includes 3.6M tonnes of overburden and waste rock resulting in a strip ratio of 7:1. |

|

12. |

The MRE presented herein is categorized as Inferred and Indicated Mineral Resources. The Inferred Mineral Resource category is constrained to areas where drill spacing is less than 150 metres and the Indicated Mineral Resource category is constrained to areas where drill spacing is less than 80 metres. In both cases, reasonable geological and grade continuity were also a criteria during the classification process. |

|

13. |

Calculations used metric units (metre, tonne). Metal contents are presented in percent, tonnes, or ounces. Metric tonnages were rounded and any discrepancies in total amounts are due to rounding errors. |

|

14. |

CIM definitions and guidelines for Mineral Resource Estimates have been followed. |

|

15. |

The QP is not aware of any known environmental, permitting, legal, title-related, taxation, sociopolitical or marketing issues, or any other relevant issues that could materially affect this MRE. |

|

16. |

The QP is not aware of any known environmental, permitting, legal, title-related, taxation, sociopolitical or marketing issues, or any other relevant issues that could materially affect this MRE. |

Table 2 below shows the sensitivity of the block model to grade cut-off. The reader is cautioned that the numbers presented in the following tables should not be misconstrued with a mineral resource statement.

Table 2 - 2023 Nisk Project Mineral Resource Estimate – Sensitivity of the block model at various cut-off grades.

|

Potential |

Cut-off Grade |

In-Situ Grade |

Calculated |

|||||

|

Class |

NiEq |

Tonnage |

Ni |

Co |

Cu |

Pd |

NiEq |

|

|

% |

t |

% |

% |

% |

g/t |

% |

||

|

Indicated |

Open Pit |

0.10 |

522,000 |

0.63 |

0.04 |

0.30 |

0.56 |

0.84 |

|

0.15 |

521,000 |

0.63 |

0.04 |

0.30 |

0.56 |

0.84 |

||

|

0.20 |

519,000 |

0.63 |

0.04 |

0.30 |

0.56 |

0.84 |

||

|

0.25 |

514,000 |

0.63 |

0.04 |

0.30 |

0.57 |

0.84 |

||

|

0.30 |

509,000 |

0.64 |

0.04 |

0.30 |

0.57 |

0.85 |

||

|

Indicated |

Underground |

0.35 |

5,211,000 |

0.76 |

0.05 |

0.40 |

0.75 |

1.03 |

|

0.45 |

5,076,000 |

0.77 |

0.05 |

0.41 |

0.77 |

1.05 |

||

|

0.55 |

4,910,000 |

0.78 |

0.05 |

0.42 |

0.78 |

1.07 |

||

|

0.65 |

4,667,000 |

0.80 |

0.05 |

0.43 |

0.80 |

1.09 |

||

|

0.75 |

4,327,000 |

0.83 |

0.05 |

0.44 |

0.83 |

1.13 |

||

|

Inferred |

Underground |

0.35 |

1,842,000 |

0.96 |

0.06 |

0.44 |

1.09 |

1.32 |

|

0.45 |

1,808,000 |

0.97 |

0.06 |

0.45 |

1.11 |

1.34 |

||

|

0.55 |

1,787,000 |

0.98 |

0.06 |

0.45 |

1.11 |

1.35 |

||

|

0.65 |

1,744,000 |

0.99 |

0.06 |

0.46 |

1.13 |

1.37 |

||

|

0.75 |

1,667,000 |

1.01 |

0.07 |

0.47 |

1.16 |

1.40 |

||

"Our inaugural NI 43-101 Technical report is an excellent start and major first step to showing the significant commercial potential of Nisk. We believe this Mineral Resource Estimate establishes us as one of the world's best nickel investment opportunities. Power Nickel took a particularly robust approach for this Mineral Resource Estimate, by involving independent experts in data management, metallurgy, mining engineering and mineral resource estimation. If compared to our peers, we may have pushed this study further than what we had to at this stage, but we believe that there is no ambiguity about the results obtained, and that this study fully supports the coming stages.", stated Power Nickel CEO Terry Lynch.

"Moving forward, Power Nickel will continue working with CVMR Inc., as they conduct a feasibility study that will review the viability of a mine at Nisk that produces not the concentrate that was modeled in this NI-43-101 but refined products. These refined products, including powders, nano powders, wires, anodes, and precursors, currently generate revenues for CVMR 2.5 to 3 times LME concentrate levels. As mentioned in the news release dated November 20th, CVMR's investment enabled Power Nickel to arrange a $2.75 million financing at a price per share twice the market price at the time, demonstrating CVMR's confidence in the Nisk mineralization. Between now and the end of Q2 2024, we anticipate continuing to drill and grow the Nisk resource and for the ongoing feasibility study to validate substantially greater recovery rates and reveal how finished products significantly improve the overall economics," added Mr. Lynch.

The Nisk deposit is magmatic Ni-Cu sulphide hosted in an elongated sill of serpentinized ultramafic rocks that intrude the Lac des Montagnes paragneiss and amphibolite sequence. The disseminated to massive Ni-Cu-Co-Fe sulphide mineralization occurs in a body of black serpentinite-altered peridotite and is typically between 5 and 15 metres thick.

An updated metallurgical test program has been completed by XPS – Expert Process Solutions, a Glencore company. XPS participated in the selection of geometallurgical samples which were tested both separately and as part of a master composite. Mineralogical and metallurgical testing was completed on the geometallurgical samples and hardness and flotation conditions were developed on the master composite. A locked cycle test was conducted on the master composite and produced a marketable concentrate containing 12.9% Ni, 4.88% Cu, 0.92% Co and 14.16 g/t Pd at recoveries of 70.0% Ni, 43.6% Cu, 78.8% Co and 66.8% Pd.

The results of the metallurgical test program were then integrated into the resource block model, enabling the calculation of a nickel-equivalent percentage (NiEq %) from the interpolated grade of nickel (Ni), copper (Cu), cobalt (Co) and palladium (Pd).

Table 3 and Table 4 present the input parameters that were used to calculate the Nickel Equivalent formula, calculate the cut-off grades, and generate the pit shell to constrain the Mineral Resources. The selling prices for Ni, Cu and Co are based on a 3-Year Average, while Pd is based on long–term pricing consensus, and the costs are benchmarked from similar operations. An exchange rate of 1.3 CAD to USD was used.

Table 3 – Input Parameters

|

Commodity |

Unit |

Price |

Recovery |

Payable |

|

Ni (3-Year Average) |

US$/lb |

10.00 |

70 % |

73 % |

|

Cu (3-Year Average) |

US$/lb |

4.00 |

44 % |

69 % |

|

Co (3-Year Average) |

US$/lb |

22.50 |

79 % |

27 % |

|

Pd (Long-Term Forecast) |

US$/oz. |

1,215 |

67 % |

78 % |

Table 4 – Economic Parameters

|

Description |

Unit |

Value |

|

Open Pit Mining Cost |

CAD/t (mined) |

5.00 |

|

U/G Mining Cost |

CAD/t (mined) |

50.00 |

|

Processing Cost |

CAD/t (milled) |

20.00 |

|

Tailings Cost |

CAD/t (milled) |

2.50 |

|

G&A Cost |

CAD/t (milled) |

5.00 |

|

Transportation Cost |

CAD/t (conc) |

185.00 |

The cut-off grade for the mineral resources within an open pit is 0.20% NiEq and 0.55% NiEq for the mineral resources for an underground mining operation. The mineral resources within an open pit do not consider mining dilution and losses. Pit slopes of 25 degrees in overburden and 45 degrees in bedrock were used to generate the pit shell. Figure 2 the Nickel Equivalent (%NiEq) grade, the mineral resource classification (indicated vs inferred), as well as the potential mining method (open pit vs underground).

"We've done an excellent job at drilling the deposit, our QPs have come up with a very robust overall study, and the deposit continues to show growth potential. Combine to this the FLEET survey and the push we've done on the geological interpretation and 3D modeling of Nisk Main, it's fair to say that we've reached a new level of geological understanding of our property, and that on many fronts. Not only it has allowed us to constrain the actual resource by its geological context, better understanding the distribution of nickel within such context has already led to developing new potential target areas. We're excited with the larger scale interpretation suggesting that Nisk Main could potentially repeat itself in adjacent structural domains. The plan is to follow that up in a very near future." – commented Kenneth Williamson, VP Exploration.

Qualified Person

Kenneth Williamson, Géo, M.Sc., VP Exploration at Power Nickel, is the qualified person who has reviewed and approved the technical disclosure contained in this news release.

About Power Nickel Inc.

Power Nickel is a Canadian junior exploration company focusing on high-potential copper, gold and battery metal prospects in Canada and Chile.

On February 1, 2021 Power Nickel (then called Chilean Metals) completed the acquisition of its option to acquire up to 80% of the Nisk project from Critical Elements Lithium Corp. (CRE:TSXV)

The NISK property comprises a large land position (20 kilometres of strike length) with numerous high-grade intercepts. Power Nickel, formerly Chilean Metals is focused on confirming and expanding its current high-grade nickel-copper PGE mineralization historical resource by preparing a new Mineral Resource Estimate in accordance with NI 43-101, identifying additional high-grade mineralization, and developing a process to potentially produce nickel sulphates responsibly for batteries to be used in the electric vehicles industry.

Power Nickel (then called Chilean Metals) announced on June 8th, 2021 that an agreement has been made to complete the 100% acquisition of its Golden Ivan project in the heart of the Golden Triangle. The Golden Triangle has reported mineral resources (past production and current resources) in total of 67 million ounces of gold, 569 million ounces of silver and 27 billion pounds of copper. This property hosts two known mineral showings (gold ore and magee), and a portion of the past-producing Silverado mine, which was reportedly exploited between 1921 and 1939. These mineral showings are described to be Polymetallic veins that contain quantities of silver, lead, zinc, plus/minus gold, and plus/minus copper.

Power Nickel is 100-per-cent owner of five properties comprising over 50,000 acres strategically located in the prolific iron-oxide-copper-gold belt of northern Chile. It also owns a 3-per-cent NSR royalty interest on any future production from the Copaquire copper-molybdenum deposit, recently sold to a subsidiary of Teck resources Inc. Under the terms of the sale agreement, Teck has the right to acquire one-third of the 3-per-cent NSR for $3-million at any time. The Copaquire property borders Teck's producing Quebrada Blanca copper mine in Chile's first region.

Neither the TSX Venture Exchange nor it's Regulation Services Provider accepts responsibility for the adequacy or accuracy of this release.

Cautionary Note Regarding Forward-Looking Statements

This message contains certain statements that may be deemed "forward-looking statements" concerning the Company within the meaning of applicable securities laws. Forward-looking statements are statements that are not historical facts and are generally, but not always, identified by the words "expects," "plans," "anticipates," "believes," "intends," "estimates," "projects," "potential," "indicates," "opportunity," "possible" and similar expressions, or that events or conditions "will," "would," "may," "could" or "should" occur. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance, are subject to risks and uncertainties, and actual results or realities may differ materially from those in the forward-looking statements. Such material risks and uncertainties include, but are not limited to, among others, the timing for the Company to close the private placement or the second Nisk option or risk that such transactions do not close at all; raise sufficient capital to fund its obligations under its property agreements going forward; to maintain its mineral tenures and concessions in good standing; to explore and develop its projects; changes in economic conditions or financial markets; the inherent hazards associates with mineral exploration and mining operations; future prices of nickel and other metals; changes in general economic conditions; accuracy of mineral resource and reserve estimates; the potential for new discoveries; the ability of the Company to obtain the necessary permits and consents required to explore, drill and develop the projects and if accepted, to obtain such licenses and approvals in a timely fashion relative to the Company's plans and business objectives for the applicable project; the general ability of the Company to monetize its mineral resources; and changes in environmental and other laws or regulations that could have an impact on the Company's operations, compliance with environmental laws and regulations, dependence on key management personnel and general competition in the mining industry.

Past performance is not an indicator of future returns. NIA is not an investment advisor and does not provide investment advice. Always do your own research and make your own investment decisions. This message is not a solicitation or recommendation to buy, sell, or hold securities. NIA has received compensation from PNPN of US$50,000 cash for a six-month marketing contract. This message is meant for informational and educational purposes only and does not provide investment advice.

Preparing Americans for Hyperinflation