Articles

NIA Update on TSX Venture Bull Market

The TSX Venture Composite Index has been in a bull market since November 10, 2023,…

Articles

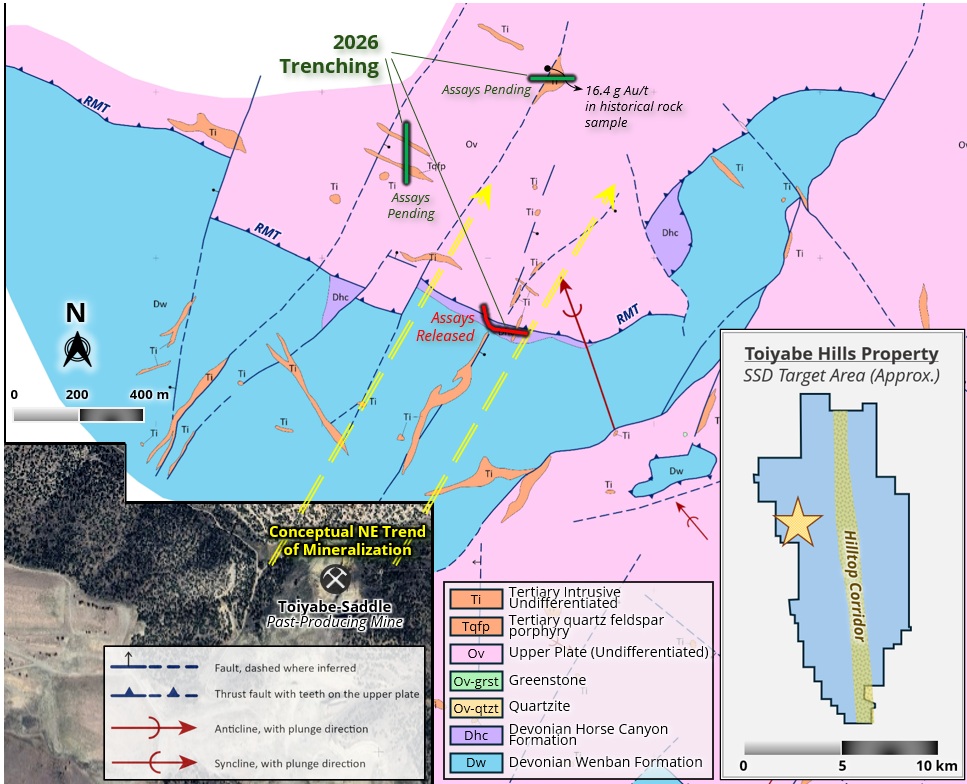

The Missing Piece of World-Class Cortez Gold District

World renowned geologist and Westward Gold (CSE: WG) Chairman Dr. Quinton Hennigh believes that WG's…

Technicals

Westward Gold Hits Another New 52-Week High

Westward Gold (CSE: WG) gained by 5.41% on Friday to $0.195 per share and hit…

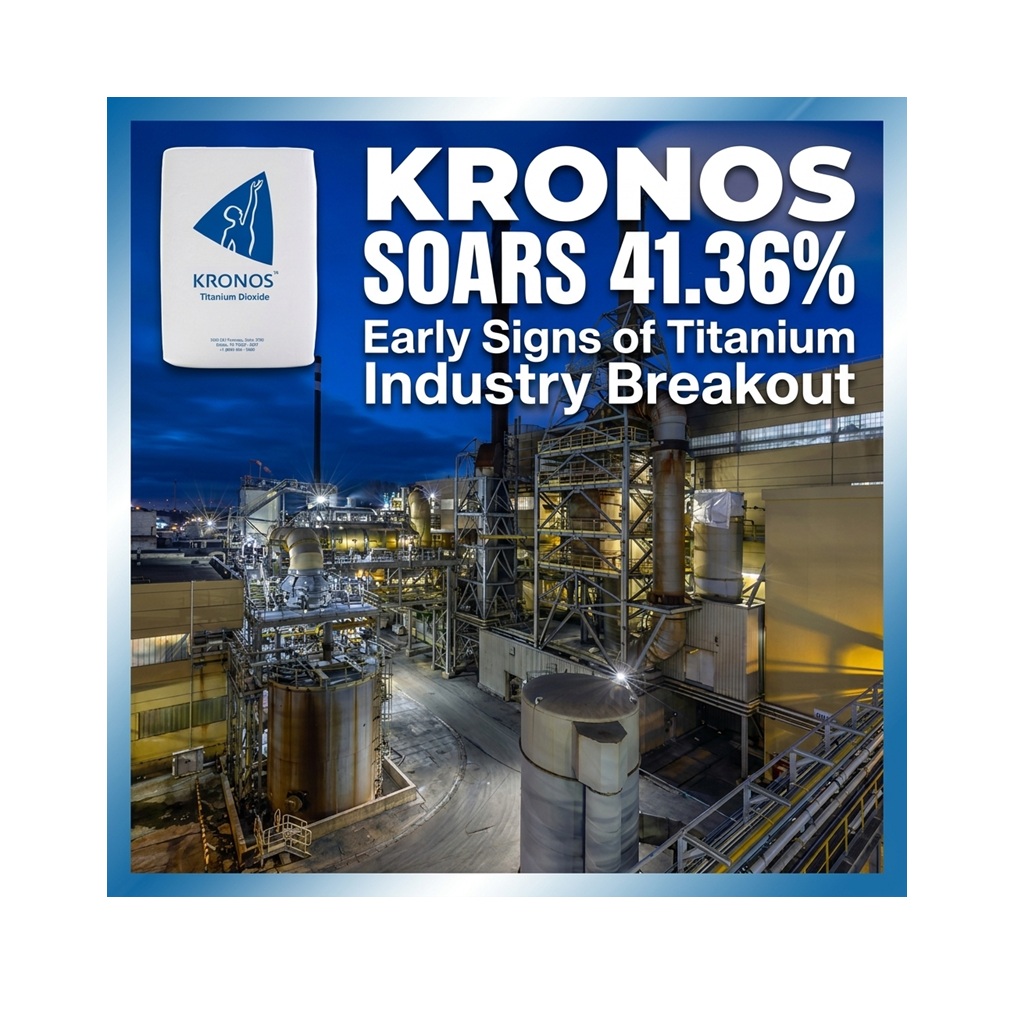

Articles

Early Signs of Titanium Industry Breakout

NIA's #1 favorite overall stock suggestion Saga Metals (TSXV: SAGA) gained by 9.28% on Friday…

Articles

Gold Up $113 to $4,353 Per Oz: Research WG and XGC Immediately

Gold is up by $113 this morning to $4,353 per oz. From what we see…

Articles

Going All-In on Titanium and Vanadium Companies

If you research companies exploring for titanium and/or vanadium it is pretty much the only…

Technicals

Westward Gold Hits New 52-Week High and New Highs Coming for First Mining

Westward Gold (CSE: WG) hit a new 52-week high today of $0.19 per share. The…

Articles

Will Trump Be Forced to Ban Chinese AI Models?

Chinese models are dominating the developer ecosystem, threatening the trillion‑dollar narratives of Anthropic and OpenAI...…

Technicals

The 2026 Fourmile Gold Rush Has Begun, Gold Up Another $118 This Morning

The 2026 Fourmile Gold Rush has just begun. Westward Gold (CSE: WG) gained by 25.93%…

Articles

New NIA Gold Stock Suggestion: Xali Gold (TSXV: XGC)

Gold is breaking out today, up $28 to $4,082 per oz, and NIA is excited to…