Announcement

QIMC Hits 23.5% Natural Hydrogen at 170 Metres

QIMC Reports Record 23.5% Natural Hydrogen Within the First 300 Metres of Ongoing DDH-26-05 and…

Articles

Huge NIA Monday Evening Update: One of NIA’s Biggest Days in History

Newmont (NEM) today agreed to pay Barrick (B) $1.95 billion in cash to add Fourmile…

Articles

NIA Update on TSX Venture Bull Market

The TSX Venture Composite Index has been in a bull market since November 10, 2023,…

Articles

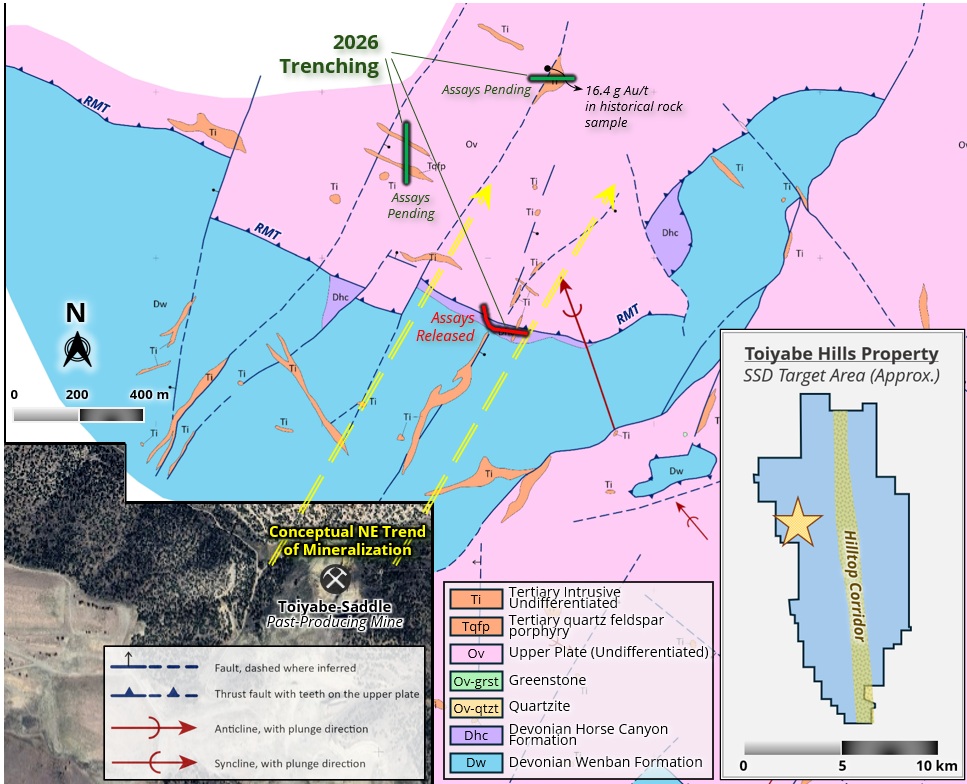

The Missing Piece of World-Class Cortez Gold District

World renowned geologist and Westward Gold (CSE: WG) Chairman Dr. Quinton Hennigh believes that WG's…

Technicals

Westward Gold Hits Another New 52-Week High

Westward Gold (CSE: WG) gained by 5.41% on Friday to $0.195 per share and hit…

Articles

Early Signs of Titanium Industry Breakout

NIA's #1 favorite overall stock suggestion Saga Metals (TSXV: SAGA) gained by 9.28% on Friday…

Articles

Gold Up $113 to $4,353 Per Oz: Research WG and XGC Immediately

Gold is up by $113 this morning to $4,353 per oz. From what we see…

Articles

Going All-In on Titanium and Vanadium Companies

If you research companies exploring for titanium and/or vanadium it is pretty much the only…

Technicals

Westward Gold Hits New 52-Week High and New Highs Coming for First Mining

Westward Gold (CSE: WG) hit a new 52-week high today of $0.19 per share. The…

Articles

Will Trump Be Forced to Ban Chinese AI Models?

Chinese models are dominating the developer ecosystem, threatening the trillion‑dollar narratives of Anthropic and OpenAI...…