Articles

How Rick Rule’s Investment into Paladin Energy Made Him $200 Million Profit

NIA Market Insight: TiO2 & Vanadium Around year 2000, Rick Rule invested in Paladin Energy…

Articles

Celtic Sign Høgh: Erling Haaland’s Worst Nightmare

Erling Haaland became the #1 biggest new football superstar in America during the World Cup,…

Articles

Exclusive NIA Report on Publicly Traded Football (Soccer) Clubs

The World's Publicly Traded Football Clubs A ranking of every publicly traded professional football (soccer)…

Articles

Huge Day for TIGR, WG, and CUPR

NIA's second-to-latest brand-new gold stock suggestion Tiger Gold (TSXV: TIGR) gained by 6.06% today after…

Articles

Christian Angermayer Will Surpass Elon Musk

With Tesla (TSLA) crashing and SpaceX (SPCX) becoming the most disastrous IPO in history, the…

Announcement

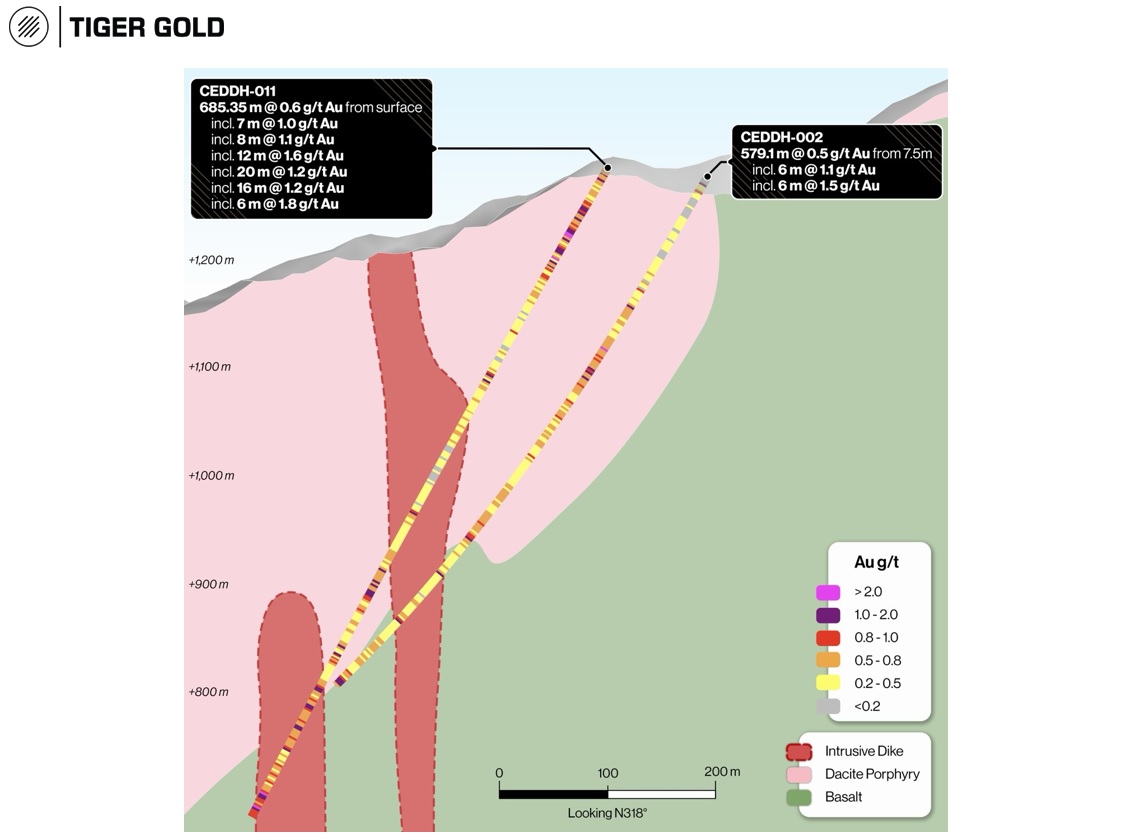

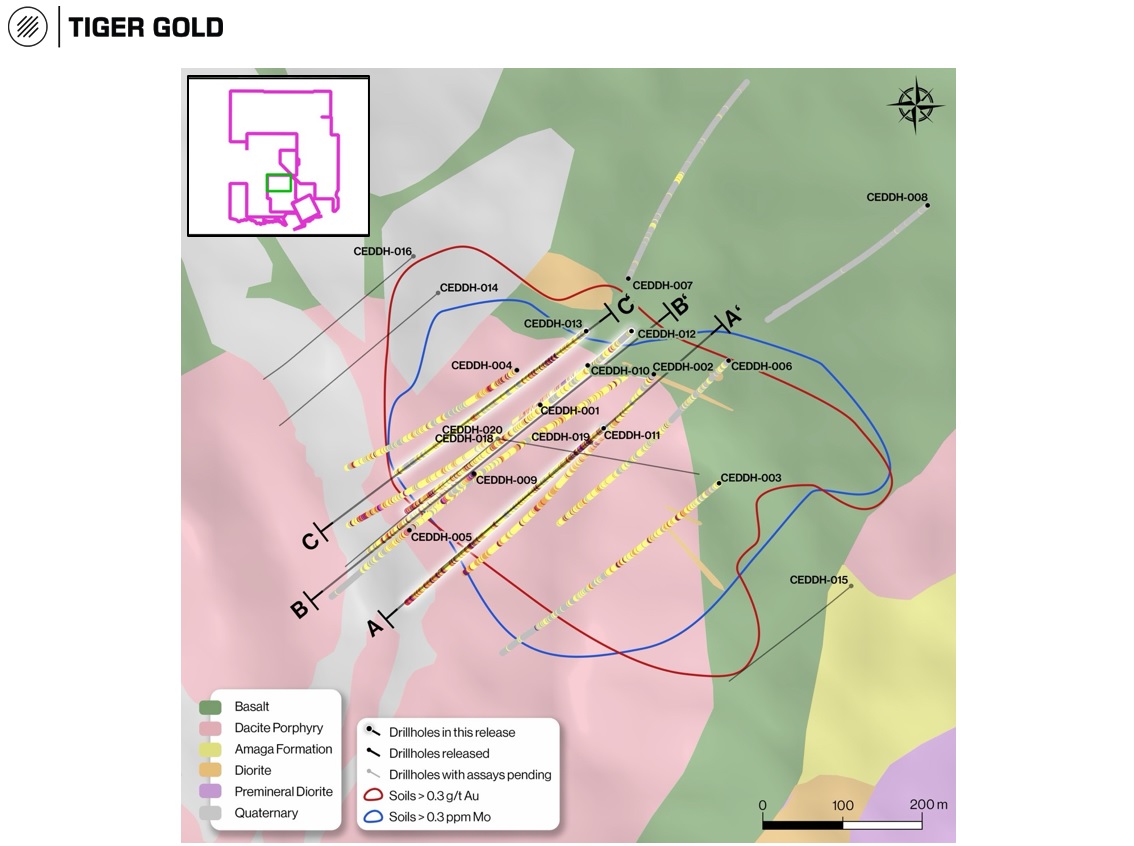

Tiger Gold Hits 685 m of Gold from Surface!

Why this matters: Tiger Gold just reported one of the longest continuous gold intervals disclosed…

Articles

Largest Titanium Bull Market in History Has Begun

Yesterday afternoon, NIA said to take a look at the titanium chemical companies that produce…

Announcement

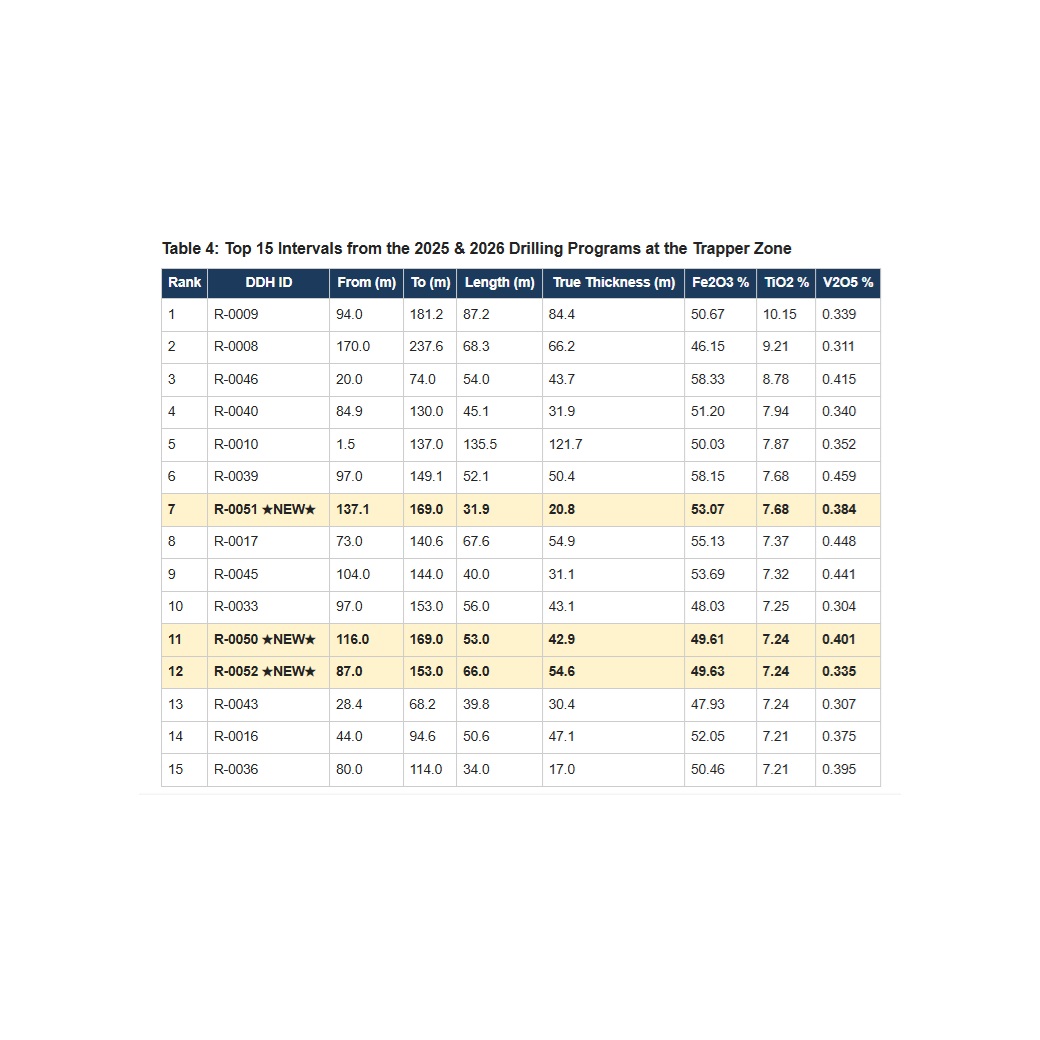

SAGA Reports 3 New Top 12 Best Drill Holes in History

🚨 Why Today's News Matters: 3 of 5 New Holes Rank Among SAGA's Top 12…

Articles

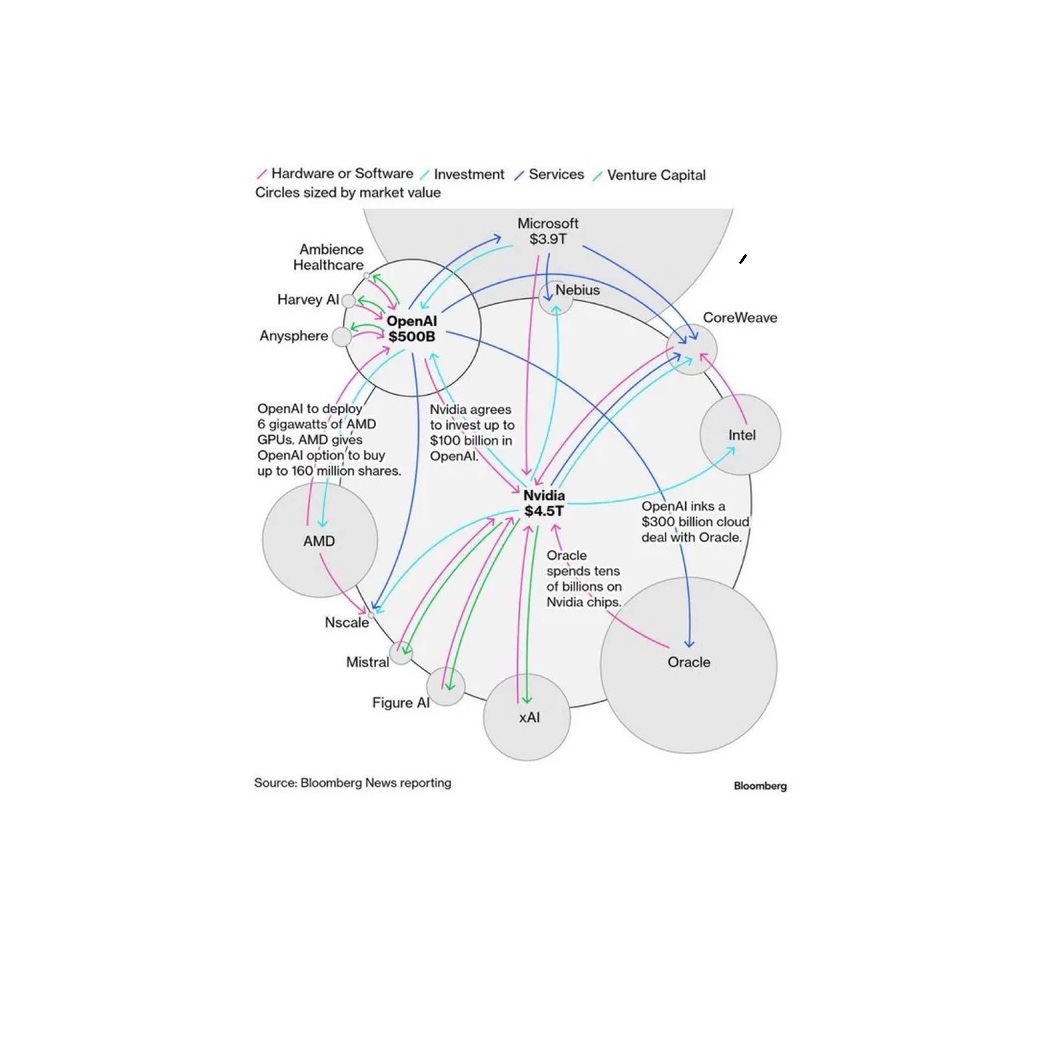

First Inning Companies to Research for AI Bubble Going Bust

AI stocks are in the 9th inning of their rally. Gold stocks are in the…

Technicals

Westward Gold Soars 12% to $0.14: Highest Close Since NIA’s Suggestion

Westward Gold (CSE: WG) gained by 12% yesterday to $0.14 per share, its highest closing…